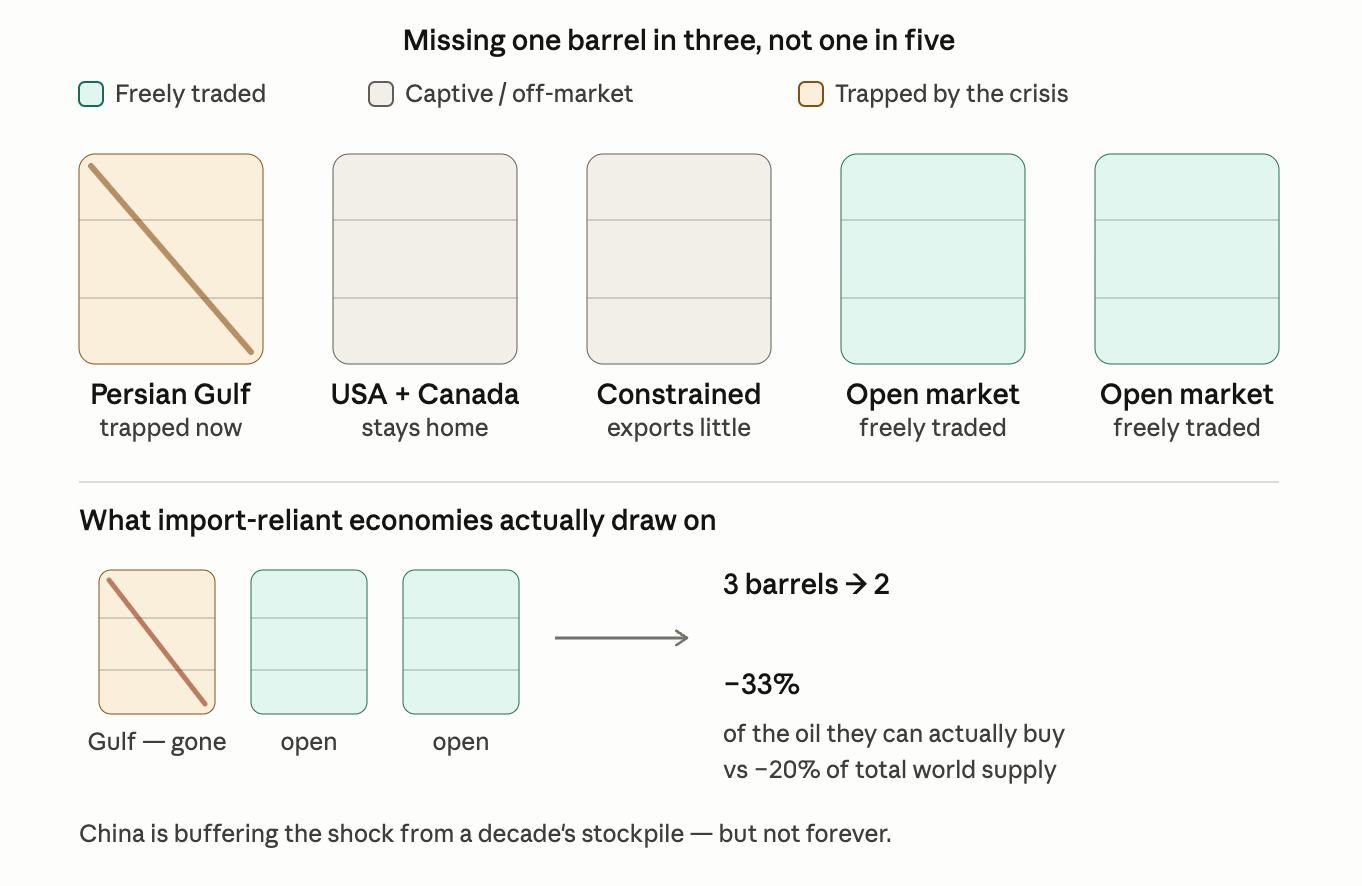

We're missing one out of three barrels of oil, not one out of five

Global oil supply is not evenly distributed, and neither will the pain of shortages be

Many people appear to be confused about why the loss of roughly 20% of the world’s oil supply is having such a dramatic effect on some countries, and a far more limited effect on others. Twenty percent is a lot, but in the news we hear of countries who may run out of some petroleum products (and derivatives) entirely. So what gives? The issue is how global oil production, and by extension supply, is distributed.

To understand this it’s helpful to frame your thinking about global oil supplies in multiples of five barrels. The whole world is painfully aware that one of those five barrels - 20% - is bottled up in the Persian Gulf by the Iran War. I’m fairly sure this will be known as the Hormuz Crisis when the history is written, but I digress.

Another whole barrel is produced by, and largely consumed by, the USA and Canada. This is why “gas” prices in the States are significantly higher but not double as they are in countries like Japan. Because the global oil market is extremely free and highly integrated, some US oil is flowing to countries like Japan, but even at the maximum feasible rate of imports it won’t replace their entire supply.

A third barrel comes from countries that either consume most of their own supply (such as the North Sea fields) or export only a fraction of what they pump (such as Brazil) or are too small to make any real difference (such as Nigeria and Venezuela). Russia is also part of this barrel, and thus its ability to supply the broader global economy is constrained by political realities.

And so we have a majority of the world’s population (including giants like India, China, Japan and Indonesia) that need to share two barrels whereas they previously had three. I’m sure we can all appreciate the difference between, for example, paying a 33% premium versus a 20% premium on something we need. An undersupply of this size is absolutely guaranteed to result in persistent physical supply shortages for these countries.

The one exception is China, which is currently living off the enormous stockpile it has accumulated over the past decade. This is why the turbulence for smaller countries like Australia and South Korea has not been as dramatic as it may have been. China is buffering the supply shock, but it cannot continue to do so forever.

There are some other details worth understanding, such as the fact that the Gulf produces a disproportionate share of petroleum byproducts like urea (46%) and helium (33%). Urea is a vital component in most fertilisers, and without it a billion or more people are likely to face a food shortage next year.

All of the above is, by virtue of the constraints of my analogy, quite oversimplified. A real oil expert will, no doubt, point out a hundred flaws in my mental model. But, at a macro scale, it’s helpful to understand that some very large countries - particularly in Asia - depend very substantially on oil flowing out of the Gulf. 85% of India’s supply comes from the Gulf, and 95% of Japan’s. Even little South Africa gets 25% of our oil from the Gulf.

When you have roughly half the world’s population competing for a scarce resource, there are going to be losers. If the standoff in the strait is not broken before the beginning of July, we should expect that many countries will implement fuel rationing and other “demand destruction” mechanisms. It’s going to be a bumpy six months.